Cloned Cards Explained: The Insider’s Guide to How Card Cloning Works & How to Spot It

Cloned Cards Aren’t Magic They’re a Simple, Brutal Form of Theft

You’ve probably seen the headlines. “Card Skimming Ring Busted.” “Hackers Steal Millions in Card Data.” Or maybe you’ve heard the term in hushed tones “cloned cards.” It sounds technical, almost futuristic. But strip away the jargon, and you’re left with a shockingly simple, mechanical crime. It’s not about hacking the mainframe in a neon-lit room. It’s about secretly copying the information off the plastic in your wallet and pasting it onto another piece of plastic.

Think of your payment card as a tiny, secure messenger. The magnetic stripe on the back is that messenger shouting your account details and name to anyone with an ear to listen. The newer EMV chip is that messenger whispering a unique, one-time code for each transaction. Cloning is the art of intercepting that shout, or less commonly, tricking that whisper.

If you’re holding your wallet a little tighter right now, good. That’s the point of this guide. Not to scare you, but to demystify the process. Because understanding how it happens is the first, most powerful step in preventing it from happening to you.

The Anatomy of a Clone: It’s All About the Data

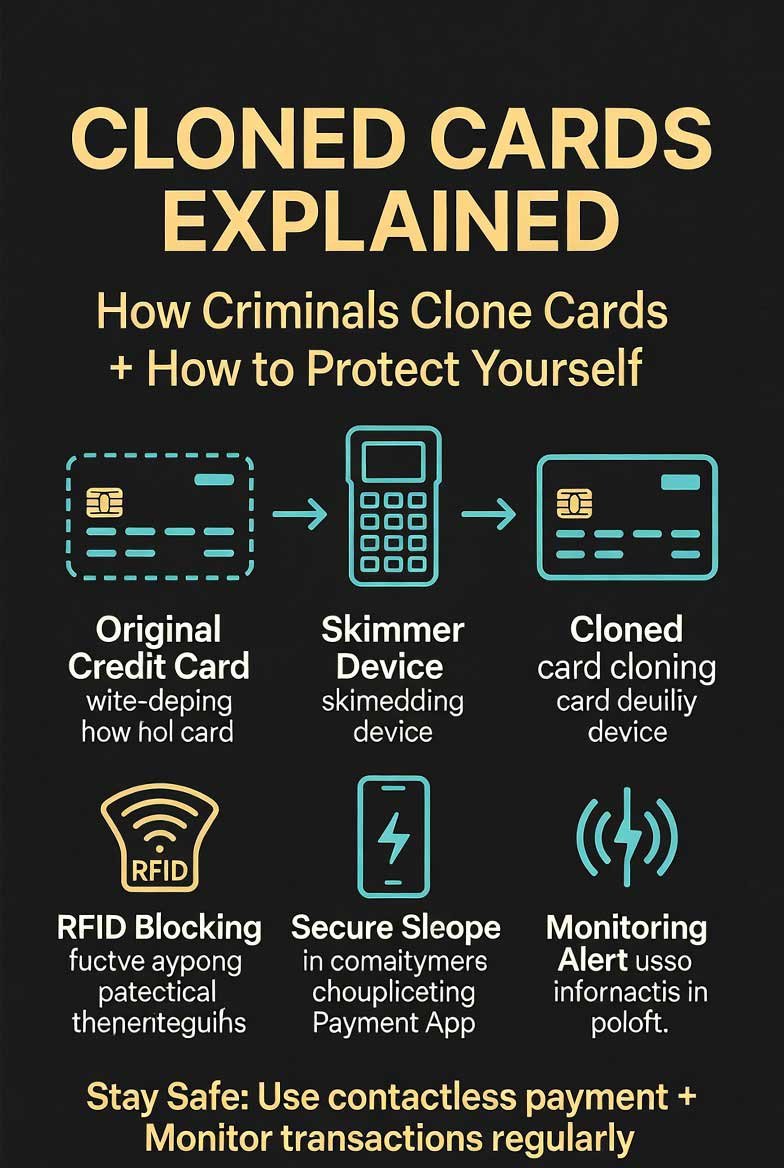

A cloned card, also called a counterfeit card, is a physical card that has been manufactured or altered to contain stolen payment card data. The clone itself is often a blank plastic card a gift card, an expired credit card, or a purpose-built blank that has been re-encoded with someone else’s information.

That information comes from two main sources on your card:

-

The Magnetic Stripe (Magstripe): This is the black or brown strip. It contains static, unchanging data tracks:

- Track 1: Your name, account number, expiration date.

- Track 2: Your account number, expiration date, and sometimes a country code (no name). This data is easy to read and copy. It’s the low-hanging fruit.

-

The EMV Chip: This is the small gold or silver square. It’s a microcomputer that generates a unique cryptographic code for each transaction. Cloning the physical chip is virtually impossible with current technology. However, criminals can sometimes intercept the data it sends during a transaction in a compromised terminal.

The key takeaway: Most “cloned cards” in circulation today are magstripe clones. They work only at terminals that still allow a magstripe swipe instead of requiring the more secure chip dip. In the US and other regions where “chip-and-signature” was common, these terminals still exist at many gas station pumps, older ATMs, and some small businesses.

How Your Card Gets Cloned: Skimmers, Shimmers, and Data Breaches

The data has to be stolen before it can be copied. Here are the main vectors:

1. Physical Skimming (The Most Common): This is a hands-on, brazen attack. A criminal installs a tiny device—a skimmer—over or inside a legitimate card reader.

- ATM/Gas Pump Skimmers: A thin, false facade is placed over the real card slot. It reads your magstripe as you insert your card. Often paired with a hidden camera or a fake keypad overlay to capture your PIN.

- POS Skimmers: A malicious employee at a restaurant or store uses a handheld skimmer (often hidden in a pocket) to swipe your card twice once for the transaction, once for the theft.

2. Shimming (The Chip Threat): A shimmer is a paper-thin device inserted inside a card reader, designed to intercept data from an EMV chip transaction. It’s more complex and rarer than skimming, but it represents the evolution of the crime to target chips. It can capture the data needed to create a functional magstripe clone.

3. Digital Skimming & Data Breaches: This is where the “hacking” part comes in. Malware is installed on point-of-sale (POS) systems in retail stores or on e-commerce payment portals. Every card swiped, dipped, or entered is logged and sent to criminals. Large-scale data breaches at retailers or payment processors can leak millions of card “dumps” (the raw data) at once.

From Data to Cash: The Carding Ecosystem

Stolen card data doesn’t just become a cloned card instantly. It moves through a well-established underground economy.

- The Data Harvesters: The skimmers, hackers, and insiders who steal the raw information.

- The Dump Sellers: They sell batches of this data (“dumps”) on dark web carding forums and markets. A “dump” includes the Track 1 & 2 data. A “dump with PIN” is far more valuable.

- The Card Manufacturers/Encoders: They buy the dumps. Using a relatively inexpensive magnetic stripe encoder (easily bought online), they write the stolen data onto blank cards. For cards with PINs, they now have everything needed to withdraw cash from an ATM.

- The Cashers or Shoppers: These are the foot soldiers. They use the physical cloned cards to withdraw cash from ATMs (known as “cashouts”) or make high-value purchases at stores for resale. They often work on a percentage cut.

The entire process, from your card being skimmed to a clone being used, can take just a few days.

FAQ: Your Pressing Questions Answered

Q: Can EMV chip cards be cloned? A: The physical EMV chip cannot be duplicated. However, the data from a chip transaction can be intercepted (via a shimmer or compromised terminal) to create a magstripe clone. This clone will only work at terminals that allow swipes. True chip cloning, where a fake chip is created, is not a practical threat currently.

Q: What’s the difference between a cloned card and card-not-present (CNP) fraud? A: A cloned card is a <em>physical counterfeit used in person. Card-Not-Present (CNP) fraud is when the stolen data (number, CVV, expiry) is used to make online or phone purchases where no physical card is needed. The same stolen data can fuel both types of fraud.

Q: How can I tell if an ATM or gas pump has a skimmer? A: Tug on it. Before inserting your card, grab the card reader fascia and give it a firm wiggle and pull. Skimmers are often loosely attached over the real reader. Check for misaligned graphics, loose parts, or anything that looks bulkier than usual. Look for hidden cameras (often in the light fixture or brochure box). When possible, use ATMs inside bank lobbies—they’re harder to tamper with.

Q: If my card is cloned, am I liable for the charges? A: In most jurisdictions (like the US under the Fair Credit Billing Act), your liability for unauthorized charges on a credit card is capped at $50 if reported promptly, and often $0. For debit cards, the rules are stricter; your liability increases the longer you wait to report. Immediate reporting is critical.

Q: Do RFID wallets protect against cloning? A: No, this is a common misconception. RFID blocking wallets prevent wireless “eavesdropping” on contactless cards (like tap-to-pay). Cloning via skimming/shimming requires physical contact with a compromised reader. An RFID wallet does nothing against a skimmer.

Your Defense Plan: How to Make Yourself a Hard Target

Criminals look for easy opportunities. A few simple habits make you a less attractive victim:

- Use the Chip, Not the Stripe: Whenever a terminal asks you to “insert” or “dip” your chip, do it. Never swipe if the chip option is available.

- Go Contactless (Tap-to-Pay): Transactions using Apple Pay, Google Pay, or a contactless card use tokenization—a one-time digital code is sent, not your actual card number. It’s more secure than even the chip for in-person buys.

- Inspect Readers & Cover Your PIN: Make the tug test a habit. Always shield the keypad with your other hand when entering your PIN, regardless of cameras.

- Monitor Your Accounts Relentlessly: Don’t wait for your monthly statement. Use your bank’s app to check transactions weekly, if not daily. Fraud alerts are your friend—turn them on.

- Use Credit Over Debit: Fraudulent charges on a credit card are the bank’s money while it’s investigated. Fraud on a debit card is your actual cash gone from your checking account until resolved.

- Gas Station Strategy: Use pumps closest to the attendant’s booth (less likely to be tampered with), or better yet, pay inside with your chip.